Field Report · 2026

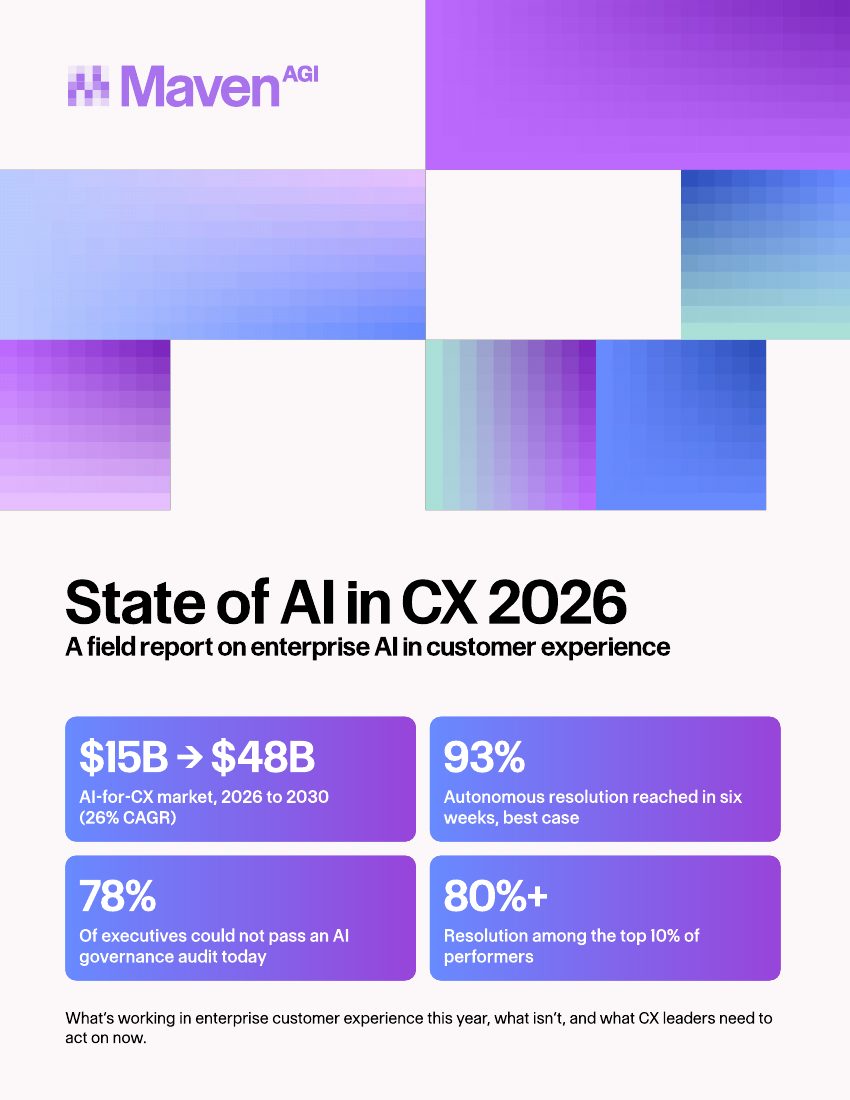

State of AI in CX 2026

A field report on enterprise AI in customer experience. What's working this year, what isn't, and what CX leaders need to act on now.

Executive Summary

01 · Executive Summary

Adoption is nearly universal.

Outcomes aren't.

The market for AI in customer experience is large and growing quickly, on track to nearly quadruple by 2030. Underneath the growth, the results aren't evenly shared. A small group of organizations run AI agents that resolve most of their customer contacts, with humans in the loop for high-priority and strategic touch points. A much larger group runs pilots that deflect a few questions and stall before they ever reach production.

This report describes four patterns that separate the two groups, drawn from third-party research and from results observed across more than 90 of Maven AGI's enterprise deployments.

The four patterns

The resolution gap

Most teams still track deflection (whether a contact avoided a human) rather than resolution (whether the problem was solved). The easier number hides reopened tickets and quietly erodes customer satisfaction.

The deployment paradox

The longest, most carefully planned rollouts tend to produce the weakest results, while tightly scoped pilots reach production in weeks. Speed applied to a narrow scope is the pattern that works.

The compliance blind spot

Governance review now stalls enterprise deals at least as often as technical fit, yet most teams treat it as a late procurement step. 78% of executives say they could not pass an independent AI governance audit today (Grant Thornton, 2026).

The voice channel opportunity

Most companies have automated chat and email and left the phone alone, even though voice is usually their highest-volume, highest-cost channel. The technical barriers have largely been resolved, and early movers are claiming a compounding cost advantage.

The report closes with the five behaviors shared by the organizations getting the best results. None of them depends on budget size or AI maturity at the start. They are operating choices, and any team can make them.

The industry has mistaken motion for progress

Spending on AI in customer service is rising fast, and nearly every contact center now uses AI in some form. Read only the adoption numbers and the story looks finished. Read the production numbers and a different picture appears. Most of that activity hasn't turned into resolved customer interactions at scale.

The distance between activity and outcome is the real story of 2026. It shows up as pilots that never graduate, dashboards that track the wrong thing, deals that stall in security review, and a phone line nobody has touched. Each of these is fixable, but none of them is fixed by deploying more.

$48B

Forecasted market size by 2030, up from ~$15B in 2026, a 26% CAGR (MarketsandMarkets)

$80B

Contact-center labor cost reduction from conversational AI in 2026 alone (Gartner)

80%

Issues agentic AI will autonomously resolve by 2029, cutting op costs ~30% (Gartner)

This report breaks that gap into four patterns: a resolution gap, a deployment paradox, a compliance blind spot, and a voice channel opportunity. Each one compounds the others. A team that measures the wrong metric will scale the wrong behavior. A team that treats compliance as a late step stalls the rollout it planned so carefully. The patterns are connected, and so are the fixes. It closes with what the organizations on the right side of the gap actually do.

"Partial integration is the dominant state of the market. It’s what happens when AI gets added to a process nobody redesigned.

02 · The State of the Market

The State of the Market

Where enterprise AI in customer experience actually stands in 2026.

The AI customer experience market is bigger, faster-growing, and more divided than the headlines suggest. Aggregate adoption numbers tell a story of universal uptake. The underlying data tells a different one: a small group of organizations are seeing compounding returns, while a much larger group runs expensive pilots that never reach production. Here are five major happenings in the 2026 market.

$48B

Forecast market size by 2030, up from ~$15B in 2026 — a 26% CAGR (MarketsandMarkets)

$80B

Contact-center labor cost reduction from conversational AI in 2026 alone (Gartner)

80%

Issues agentic AI will autonomously resolve by 2029, cutting op costs ~30% (Gartner)

01

The headline figure is real.

The market for AI in customer service was valued at roughly $15B in 2026 and is forecast to reach $48B by 2030, a 26% compound annual growth rate (MarketsandMarkets). Investment is climbing sharply, and the projected savings are even larger: Gartner expects conversational AI to cut contact-center labor costs by about $80B in 2026 alone. Production-scale deployments are not keeping pace with the spending.

02

Most generative AI projects never reach production.

By one widely cited MIT estimate from 2025, roughly 95% of enterprise generative AI pilots fail to reach measurable business impact at scale. The exact figure is debated; the direction is not. The failure point is rarely the model. It is data access, escalation design, and unclear ownership inside the buying organization.

03

“Partial integration” is the dominant state.

Around 88% of contact centers now use AI in some capacity, but only about a quarter have fully integrated it into daily operations (industry data, 2026). Partial integration means deflection works in narrow paths and resolution does not happen at scale.

04

The governance gap is widening.

In April 2026, Grant Thornton reported that 78% of executives could not pass an independent AI governance audit today. Compliance has moved from a procurement checkbox to a deployment gate, a theme Section 5 returns to.

05

The top performers are pulling away.

Across the deployments behind this report, the top 10% of performers see 80% or higher autonomous resolution, while the median sits well below that. The gap is widening, the clearest sign that outcomes track how AI is run rather than whether it was adopted. Gartner projects that by 2029, agentic AI will autonomously resolve 80% of common customer service issues. Today's top performers are early to a curve the whole category is on.

Read only the adoption numbers and the story looks finished. Read the production numbers and a different picture appears.

What this looks like on the ground

Consider a familiar arc. An enterprise CX leader deploys an AI tool in early 2025, watches it handle a narrow band of simple questions, and reports a strong deflection number to the executive team. Within four months the deflection rate plateaus, repeat contacts climb, and satisfaction slips on exactly the interactions the tool was supposed to own. By late 2025 the team rebuilds around resolution rather than deflection, and the numbers that matter start to move. This pattern is common enough across deployments to treat it as the default path, not the exception.

The organizations that skip the detour share one early choice: they build the dashboard around resolution before the agent goes live, not after the numbers disappoint. In the strongest case in Maven's data, one customer reached 93% autonomous resolution within six weeks by holding the program to that single question from the start.

So, why is the most important metric in AI customer service the one most vendors don't report?

03 · The Resolution Gap

The Resolution Gap

Why the most important metric in AI customer service is the one most vendors don't report.

Of the two numbers, the industry optimized for the easier one. Deflection is simple to count and flattering to report, so it became the default. The trouble is that deflection and resolution can move in opposite directions: a ticket can be closed and still leave the customer's problem unsolved. That gap is where AI either earns its return or quietly cannibalizes satisfaction. Independent analysts have started drawing the same line, treating deflection, containment, resolution, and first-contact resolution as four distinct measures precisely because they diverge in practice.

Deflection

Did the ticket leave the queue?

Easy to count and inherited from the rule-based bot era. A contact either touches a human or it doesn't, but it hides the reopen rate. A contact deflected and back within 48 hours counts as deflected once and resolved zero times.

Resolution

Did the customer leave satisfied?

Harder to report because it is honest about reopens and satisfaction, not just routing. It requires actually defining what "solved" means, and any team serious about it can state a number.

Framework

The True Resolution Formula

A contact counts as resolved only when all three conditions hold. Each condition catches a different failure mode. A director can sketch this on a whiteboard in the next team meeting and re-score last month's data against it without buying anything.

1

Closed without escalation

The AI agent completed the request autonomously. Catches contacts the agent could not handle.

2

No reopen within X timeframe

The customer didn't come back about the same issue within a predetermined window, commonly 7 days, though many organizations set it by their own satisfaction goals. Catches answers that looked complete but weren't.

3

No negative CSAT

The customer did not rate the interaction poorly. Catches contacts that were technically closed and quietly infuriating.

Maven's top deployments reach 80% to 93% resolution by month six. These programs connected the AI agent to systems of record from day one and measured resolution against the formula above, not deflection. In one fintech deployment, the agent reached 90% autonomous resolution within three weeks. A legal-technology company that evaluated 32 vendors and stress-tested more than ten of them measured 60% more tickets solved after switching from a rule-based system to autonomous resolution.

90%

Autonomous resolution in 3 weeks, fintech deployment

+60%

More tickets solved after moving from rules to autonomous resolution

80–93%

Resolution reached by top deployments by month six

Ask for the resolution rate, not the deflection rate. Resolution is harder to report than deflection because it is honest about reopens and satisfaction, not just routing. Any team serious about it can state a number. Treat a number you cannot get as a data point in itself.

Deflection measures whether a ticket left the queue. Resolution measures whether the customer left satisfied.

04 · The Deployment Paradox

The Deployment Paradox

Why companies that move fast outperform companies that plan carefully, and why fast without a tight scope is the most expensive mistake of all.

The longest deployments tend to produce the worst outcomes. Organizations that spend 12 to 18 months on vendor selection, procurement, and planning typically launch to lower resolution rates than companies that ran a tightly scoped pilot in 90 days. However, speed is not a tactic. Speed with a narrow scope is a strategy. The caution is real, though: speed applied to a process that was never redesigned for AI generates new categories of failure at scale, which is why scope matters as much as pace.

The 12-to-18-month timeline is a procurement artifact, not a product requirement. It exists because RFPs, security reviews, and integration planning get run one after another when they could run in parallel. The broader failure data points the same way: McKinsey finds that while nearly every company now uses AI in some form, only about 1% describe their deployments as mature, and RAND has put the AI project failure rate near 80%, well above other IT work. The constraint is organizational readiness, not the model.

Three decisions account for most deployment delays: data access, compliance sign-off, and escalation design. Running these in parallel rather than in series is the single biggest lever on how long a deployment takes. For Maven deployments, it tends to be the difference between a quarter and a year.

Framework

The 90-Day Pilot Scope

A reference scope for a 500-seat CX organization that wants to prove resolution before a broad rollout:

1

One channel

Start where volume and intent are most predictable, usually chat or email.

2

One customer segment

A defined population, not the whole base.

3

One intent cluster

A well-bounded set of related requests, not "everything."

Pre-build the escalation rules, define success criteria up front (resolution against the formula in Section 3), and set a six-week measurement window. The pilot proves the resolution rate, and the proof unlocks the broader rollout. Scope is what keeps speed safe.

05 · The Compliance Blind Spot

The Compliance Blind Spot

Why security and compliance requirements stall more deployments than technology does.

The conversation about AI in customer service is dominated by capability questions. Can the agent handle complex queries? Can it understand context? The question that gets forgotten is whether the platform can pass a security and compliance review without forcing a rewrite of the deployment plan. In 2026, that is the question that decides timelines.

Compliance is now the primary bottleneck in enterprise AI procurement. In our experience, and consistent with what governance researchers report, security review now stalls enterprise deals at least as often as technical fit, and usually after the technical evaluation has already gone well. The friction is widely felt: BCG reports that 74% of enterprises struggle to balance innovation with security when deploying generative AI. Buyers who don't pre-stage the compliance conversation typically lose two to three months in mid-funnel.

78%

of executives could not pass an independent AI governance audit today (Grant Thornton, Apr 2026)

74%

of enterprises struggle to balance innovation with security (BCG)

2–3

months typically lost in mid-funnel when compliance is not pre-staged

The certification landscape has consolidated

SOC 2, HIPAA, GDPR, and PCI-DSS 4.0 are table stakes for any vendor handling regulated data. ISO 42001, the AI-specific governance standard, is the new differentiator, and most vendors don't hold it yet. The shift mirrors what happened with SOC 2 and ISO 27001 a decade ago. By one 2026 survey, a large majority of Fortune 500 procurement teams plan to require ISO 42001 alignment from vendors by 2027. The most rigorously certified platforms now hold at least ten certifications and assessments, ISO 42001 among them.

Two requirements are moving from optional to decisive. PCI on live voice calls (real-time redaction, audit trails, segmented handling) is becoming a shortlist filter as voice handles more payment data, and most voice products were not architected for it. Data residency by region decides whether a vendor can even be considered in financial services, healthcare, and parts of EMEA and APAC. Both belong in early screening, not late legal review.

Framework

The AI Compliance Buyer's Checklist

"We are compliant" is not a claim a buyer can evaluate. These are the questions that make it specific. Ask every vendor:

1

Which certifications, and what scope?

Names alone are not enough; scope and audit dates are.

2

When was the last audit, and who performed it?

Recency and independence both matter.

3

Do you hold ISO 42001?

The AI-specific governance standard, not a general security cert.

4

How is PCI handled on a live voice call?

Real-time redaction, audit trail, segmentation.

5

What data residency options exist?

By region, with specifics.

6

Can we run our own penetration test?

A yes signals confidence; a no is informative.

Proof that the bar is clearable. A Fortune 500 gaming enterprise runs more than 330,000 monthly interactions on an autonomous AI agent under regulated-industry constraints, which in that sector means both PCI compliance for in-game purchases and AML and KYC handling. An organization facing that level of scrutiny scaled rather than stalled, which is the point: compliance depth is a gate that can be passed early when the platform is built for it.

The most consequential deployment decision is the dashboard you build before going live.

06 · The Voice Channel Opportunity

The Voice Channel Opportunity

The channel most companies have not automated.

Voice is the highest-volume, highest-cost, and most technically complex channel in customer service. It's also the channel where AI adoption lags furthest behind. That gap is closing fast: industry forecasts put the voice AI market growing at roughly a 35% annual rate, faster than the broader category, and one 2026 tracker counted a 340% year-over-year jump in production voice deployments across more than 500 organizations (Opus Research). The organizations that move early hold a cost advantage that compounds quarter over quarter.

340%

Year-over-year jump in production voice AI deployments (Opus Research, 2026)

~35%

CAGR for the voice AI market, faster than the broader category

500+

Organizations tracked with production voice deployments

Voice lagged for three real reasons, and all three are now solvable

Barrier

What it meant on a live call

Status in 2026

Latency

Sub-300ms response is non-negotiable on a live call.

Solved in production

Accuracy

Recognition across accents and overlapping speech.

Solved

Compliance

Requirements stricter than text, PCI on live calls.

Solved when built for it

None of these were solvable in 2023, in 2026 they are. Enterprise voice is a different product than consumer voice: multilingual handling at the level of 50+ languages, PCI compliance on live calls, sub-300ms response in production, and integration with existing telephony. The bar is higher and the field of vendors that clear it is much smaller.

Voice is closing the gap with chat. The assumption that voice is fundamentally harder to automate is largely a 2023 artifact. In the deployments Maven has measured, well-built voice agents resolve in the same range as chat on comparable intents. The complexity is real, but it's bounded, a short set of decisions, not the technology, now sets deployment speed.

Framework

The Voice AI Deployment Decision Tree

Three decisions, two defensible defaults each, mapped to deployment speed and ROI. For most enterprise buyers, the faster default in each row is also the safer one.

1

Telephony

Faster · preferred — Integrate with the existing carrier and stack. · Slower — Migrate: rarely worth it first.

2

IVR

Lower risk — Integrate with the existing carrier and stack. · Longer path — Replace it: higher ceiling.

3

Escalation

Preferred — Warm handoff to a human with full context. · Avoid — Cold handoff.

This framework pairs with the 90-Day Pilot Scope in Section 4 for teams considering voice as their first automated channel.

In 2026, compliance is the gate. The vendor that produces its certification scope and audit dates first usually wins the security review.

07 · What the Top 10% Get Right

What the Top 10% Get Right

A synthesis of what separates deployments that work from deployments that do not.

Across the deployments behind this report, the same pattern shows up among the organizations getting exceptional outcomes, and it has little to do with budget size or technical sophistication at the start. It comes down to how the buying organization runs the program after a vendor is chosen. Four of the five behaviors below were argued in the sections above; collected here, they read as a single operating model. The fifth is the one most teams skip.

The five behaviors of top performers

01

Measure resolution, not deflection, from day one.

The dashboard is built before the first agent goes live, not bolted on after the numbers disappoint.

02

Start narrow and expand on proof.

A scoped pilot earns the rollout; nobody waits for a perfect roadmap.

03

Overlay before migrating.

Connect AI to the systems that already exist rather than letting an ideal architecture block a working deployment.

04

Certify before scaling.

Compliance gates expansion, not the pilot, which avoids the most expensive retrofit in enterprise AI.

05

Run the agent as a product, not a project.

Resolution and reopen data reviewed weekly, intent coverage quarterly. This is the behavior the earlier sections don't cover, and the one most teams skip.

The next 18 months

Agentic AI is moving from advisory to operational, from suggesting answers to completing tasks. The agent-to-agent era is beginning, where AI agents hand off to other specialized agents. The organizations building institutional knowledge about single-agent deployment now will be substantially ahead when the multi-agent stacks arrive in late 2026 and 2027.

Three things to watch through H2 2026

Why it matters

ISO 42001 consolidates — from differentiator into procurement requirement

Accelerated as EU AI Act obligations for higher-risk systems take effect across 2026–2027.

PCI compliance for voice — becomes a standard shortlist filter

As voice handles more payment data, unarchitected products get filtered out early.

Resolution rate emerges — as a published industry metric

Analyst language has moved: Gartner frames its 2029 milestone as autonomous resolution, not deflection.

What made voice hard in 2023 was latency, accents, and compliance. Those are now engineering problems with answers.

08 · Where to Start

Where to start

None of the five behaviors requires a budget approval. The first one, measuring resolution instead of deflection, can be done this quarter against data a team already has. The True Resolution Formula in Section 3 is the place to begin: re-score last month's contacts on whether they closed without escalation, stayed closed for a specific amount of time that works for your customer satisfaction standards, and avoided a negative rating. The gap between that number and the deflection rate on the current dashboard is the size of the opportunity.

Do this first

Start this quarter, with data you already have

1

Re-score last month's contacts against the True Resolution Formula

Closed without escalation, no reopen within your window, no negative CSAT.

2

Compare that resolution number to the deflection rate on your current dashboard.

3

The gap between them is the size of your opportunity.

This report was produced by Maven AGI, drawing on production data from more than 90 enterprise deployments of autonomous AI agents across chat, voice, and email.

Selected sources

Third-party research cited in this report

Gartner — agentic AI customer service forecast (2025): by 2029, agentic AI will autonomously resolve 80% of common customer service issues without human intervention, cutting operating costs by roughly 30%.

Gartner — conversational AI cost outlook: roughly $80B in contact-center labor cost reduction in 2026.

Gartner — AI governance procurement survey (2026): a large majority of Fortune 500 procurement teams plan to require ISO 42001 alignment from vendors by 2027.

MarketsandMarkets — AI for Customer Service Market forecast: $12.06B (2024) to $47.82B (2030), 25.8% CAGR; roughly $15B in 2026.

MIT (2025): a large majority of enterprise generative AI pilots, by one widely cited estimate around 95%, fail to reach measurable business impact at scale.

McKinsey: near-universal AI use, with only about 1% of organizations describing their deployments as mature.

RAND: AI project failure rate near 80%, above other IT work.

Grant Thornton (April 2026): 78% of executives could not pass an independent AI governance audit today.

BCG: 74% of enterprises struggle to balance innovation with security when deploying generative AI.

Opus Research (2026): roughly 340% year-over-year growth in production voice AI deployments across more than 500 organizations; voice AI market growing at about a 35% CAGR by 2026 forecasts.

Industry contact-center data (2026): roughly 88% of contact centers use AI in some capacity, but only about a quarter have fully integrated it.

Continue reading

Read the full report

Enter your email to unlock the complete State of AI in CX 2026 report right here on this page, and we'll send the full PDF to your inbox.

✓

The Resolution Gap & the True Resolution Formula

✓

The 90-Day Pilot Scope & Compliance Buyer's Checklist

✓

The five behaviors of top-10% performers

✓

Benchmarks from 90+ enterprise deployments

We'll email you the full PDF and unlock it here instantly. By submitting, you agree to Maven AGI's Privacy Policy. We never sell your data.

See what 80–93% resolution looks like

Maven AGI runs autonomous AI agents across chat, voice, and email for 90+ enterprises. Bring your data and we'll show you the resolution gap in your own numbers.

Book a demo →